Federal Student Loan Repayment Plans 2026: A Comprehensive Comparison

Understanding and choosing the right Student Loan Repayment Plans can feel like navigating a labyrinth. For millions of Americans, federal student loans represent a significant financial commitment, and selecting the optimal repayment strategy is crucial for long-term financial health. As we look towards 2026, it’s more important than ever to be informed about the various federal options available, especially with recent changes and ongoing discussions around student loan policy.

This comprehensive guide aims to demystify the primary federal student loan repayment plans: the new SAVE Plan, Pay As You Earn (PAYE), Income-Based Repayment (IBR), and Income-Contingent Repayment (ICR). We’ll delve into the nuances of each, helping you compare their features, understand their eligibility requirements, and ultimately, determine which plan aligns best with your financial situation and goals. Whether you’re a recent graduate, an established professional, or someone experiencing financial hardship, optimizing your repayment strategy is key to managing your student debt effectively.

The Importance of Choosing the Right Student Loan Repayment Plans

Before diving into the specifics of each plan, let’s briefly discuss why this decision holds such weight. Your choice of Student Loan Repayment Plans directly impacts your monthly payments, the total amount you repay over time, potential eligibility for loan forgiveness, and even your credit score. A well-chosen plan can alleviate financial stress, free up funds for other life goals, and provide a clear path to debt freedom. Conversely, a mismatched plan can lead to missed payments, accumulating interest, and a prolonged struggle with debt.

The landscape of federal student loans is dynamic. Policies can shift, and new programs can emerge, making continuous education essential. Our focus here is on the plans most relevant for borrowers looking ahead to 2026, ensuring you have the most current and actionable information at your fingertips.

Understanding the Standard Repayment Plan: The Baseline

While not an income-driven plan, the Standard Repayment Plan serves as the baseline against which all other plans are measured. It’s automatically assigned to most federal loan borrowers unless they actively choose another option.

Standard Repayment Plan: Key Features

- Fixed Payments: Your monthly payment is fixed for the life of the loan.

- 10-Year Term: Loans are typically paid off within 10 years (or 10 to 30 years for consolidated loans).

- Lowest Total Cost: Generally results in the lowest total interest paid over the life of the loan because you pay it off fastest.

- Eligibility: All federal student loan borrowers are eligible.

Who is the Standard Plan Best For?

This plan is ideal for borrowers who can comfortably afford the monthly payments and want to pay off their loans as quickly as possible to minimize interest accrual. If your income is stable and sufficient, the Standard Repayment Plan offers the most straightforward and often the cheapest path to debt freedom.

Deep Dive into Income-Driven Repayment (IDR) Plans

Income-Driven Repayment (IDR) plans are designed to make federal student loan payments more affordable by basing them on your income and family size. These plans are a lifeline for borrowers struggling to meet their monthly obligations under the Standard Plan. While they often extend the repayment period, they also offer the possibility of loan forgiveness after a certain number of years.

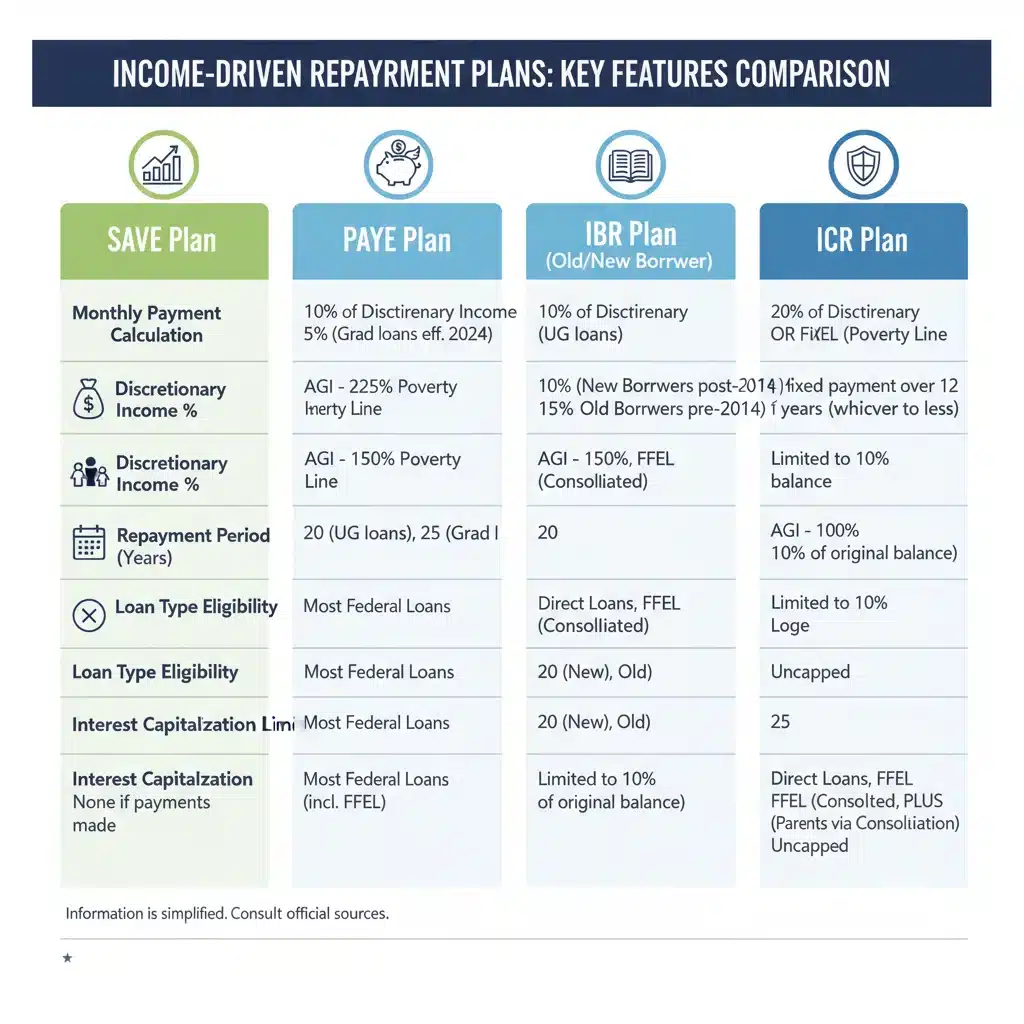

1. The SAVE Plan (Saving on a Valuable Education): A Game Changer for 2026

The SAVE Plan, which fully rolled out in July 2024, is a significant overhaul of the previous Revised Pay As You Earn (REPAYE) plan and is set to be a cornerstone of federal Student Loan Repayment Plans for 2026 and beyond. It offers the most generous terms for many borrowers.

SAVE Plan: Key Features and Benefits

- Payment Calculation: Monthly payments are calculated based on a percentage of your discretionary income. For undergraduate loans, payments will be 5% of discretionary income (down from 10% on REPAYE). For graduate loans, it remains 10%, and for borrowers with both undergraduate and graduate loans, it’s a weighted average.

- Discretionary Income Definition: Discretionary income is defined as the difference between your adjusted gross income (AGI) and 225% of the federal poverty guideline for your family size (an increase from 150% for other IDR plans). This means more of your income is protected, leading to lower monthly payments for many.

- Interest Subsidy: A major benefit is that if your calculated monthly payment doesn’t cover the full amount of interest due, the government covers the remaining interest. This prevents your loan balance from growing due to unpaid interest, a common issue with other IDR plans.

- Loan Forgiveness: Forgiveness is available after 10 years of payments for original loan balances of $12,000 or less. For every $1,000 borrowed above that, an additional year of payments is added, up to a maximum of 20 years for undergraduate loans and 25 years for graduate loans.

- Spousal Income Exclusion: If you’re married and file separately, your spouse’s income is NOT included in the payment calculation, which can significantly lower payments for some.

- Automatic Enrollment: Borrowers previously on REPAYE were automatically transitioned to SAVE.

Who is the SAVE Plan Best For?

The SAVE Plan is particularly beneficial for:

- Borrowers with low to moderate incomes, especially those with undergraduate loans.

- Individuals whose monthly payments under other plans would not cover their accruing interest, as the interest subsidy prevents balance growth.

- Married borrowers who file taxes separately and wish to exclude spousal income.

- Those seeking the fastest path to loan forgiveness for smaller loan balances.

2. Pay As You Earn (PAYE) Repayment Plan

The PAYE plan is another popular IDR option, offering lower monthly payments for many eligible borrowers. However, it has stricter eligibility requirements compared to IBR or ICR.

PAYE Plan: Key Features

- Payment Calculation: Monthly payments are generally 10% of your discretionary income, but never more than what you’d pay under the Standard Repayment Plan.

- Discretionary Income Definition: Discretionary income is the difference between your AGI and 150% of the federal poverty guideline for your family size.

- Loan Forgiveness: Any remaining balance is forgiven after 20 years of qualifying payments.

- Eligibility: To qualify, you must be a ‘new borrower’ as of October 1, 2007, meaning you had no outstanding balance on a Direct Loan or FFEL Program loan when you received a Direct Loan or FFEL Program loan on or after that date. You also must have received a new Direct Loan on or after October 1, 2011. Additionally, you must demonstrate a ‘partial financial hardship.’

- Interest Capitalization: If you no longer have a partial financial hardship, or if you leave the PAYE plan, unpaid interest may capitalize, increasing your principal balance. However, there’s a cap on how much interest can capitalize (it won’t exceed 10% of your original principal balance).

Who is the PAYE Plan Best For?

PAYE is a strong option for:

- Newer borrowers with a high debt-to-income ratio.

- Borrowers who want lower payments but are also concerned about the potential for interest capitalization, as PAYE has a cap.

- Those who anticipate their income increasing over time and want the protection of payments never exceeding the Standard Plan amount.

3. Income-Based Repayment (IBR) Plan

IBR was one of the first IDR plans and remains a viable option for many borrowers, especially those who don’t qualify for PAYE or SAVE due to eligibility restrictions.

IBR Plan: Key Features

- Payment Calculation: Payments are either 10% or 15% of your discretionary income, depending on when you took out your loans, but never more than what you’d pay under the Standard Repayment Plan.

- Discretionary Income Definition: Discretionary income is the difference between your AGI and 150% of the federal poverty guideline for your family size.

- Loan Forgiveness: Forgiveness is granted after 20 or 25 years of qualifying payments, depending on when you borrowed.

- Eligibility: You must demonstrate a ‘partial financial hardship.’ This is generally easier to meet than PAYE’s ‘new borrower’ requirement.

- Interest Capitalization: If you no longer have a partial financial hardship, or if you leave the IBR plan, unpaid interest may capitalize. There is no cap on the amount of interest that can capitalize under IBR, which can be a significant drawback.

Who is the IBR Plan Best For?

IBR is suitable for:

- Borrowers who don’t meet the ‘new borrower’ criteria for PAYE or SAVE.

- Those with high debt relative to their income who need lower monthly payments.

- Borrowers who anticipate a long repayment period and are pursuing Public Service Loan Forgiveness (PSLF) or other forgiveness programs.

4. Income-Contingent Repayment (ICR) Plan

The ICR plan is often considered the least generous of the IDR options, but it has the broadest eligibility and can be a fallback for those who don’t qualify for other plans.

ICR Plan: Key Features

- Payment Calculation: Your monthly payment will be the lesser of: 20% of your discretionary income, or what you would pay on a fixed 12-year repayment plan, adjusted according to your income.

- Discretionary Income Definition: Discretionary income is the difference between your AGI and 100% of the federal poverty guideline for your family size. This means a smaller portion of your income is protected, potentially leading to higher payments compared to other IDR plans.

- Loan Forgiveness: Any remaining balance is forgiven after 25 years of qualifying payments.

- Eligibility: All Direct Loan borrowers are eligible, regardless of when they borrowed or their income. It’s also the only IDR plan available for Parent PLUS Loan borrowers who consolidate their loans.

- Interest Capitalization: Unpaid interest may capitalize, but it’s capped at 10% of your original principal balance.

Who is the ICR Plan Best For?

ICR is primarily recommended for:

- Parent PLUS Loan borrowers who have consolidated their loans.

- Borrowers who do not qualify for other IDR plans due to specific eligibility requirements.

- Those who want the flexibility of an income-driven plan but have higher incomes that might make other IDR plans less advantageous.

Comparing the Federal Student Loan Repayment Plans: A Side-by-Side Look for 2026

To help solidify your understanding, let’s look at a comparative overview of these Student Loan Repayment Plans, keeping 2026 in mind.

| Feature | SAVE Plan | PAYE Plan | IBR Plan | ICR Plan |

|---|---|---|---|---|

| Payment Calculation | 5% (undergrad), 10% (grad) of discretionary income | 10% of discretionary income | 10% or 15% of discretionary income (based on loan date) | 20% of discretionary income or 12-year fixed, whichever is less |

| Discretionary Income Threshold | AGI – 225% Poverty Line | AGI – 150% Poverty Line | AGI – 150% Poverty Line | AGI – 100% Poverty Line |

| Payment Cap | No cap based on Standard Plan | Never more than Standard Plan | Never more than Standard Plan | No cap based on Standard Plan |

| Interest Subsidy | Government covers unpaid interest | Limited subsidy (if payments don’t cover interest) | Limited subsidy (if payments don’t cover interest) | No specific interest subsidy beyond payment calculation |

| Forgiveness Term | 10-25 years (based on original loan amount) | 20 years | 20 or 25 years (based on loan date) | 25 years |

| Eligibility | Direct Loans, FFEL (consolidated) | Direct Loans, ‘new borrower’, partial financial hardship | Direct Loans, FFEL, partial financial hardship | Direct Loans, FFEL (consolidated), Parent PLUS (consolidated) |

| Married, Filing Separately | Spouse’s income excluded | Spouse’s income excluded | Spouse’s income excluded | Spouse’s income included |

Important Considerations When Choosing Your Student Loan Repayment Plans

Public Service Loan Forgiveness (PSLF)

If you work for a government agency or a qualifying non-profit organization, the Public Service Loan Forgiveness (PSLF) program could be a game-changer. Under PSLF, your remaining loan balance is forgiven after 120 qualifying monthly payments (10 years) while working full-time for a qualifying employer. Payments made under any IDR plan (SAVE, PAYE, IBR, ICR) qualify for PSLF. This makes choosing an IDR plan even more critical if you’re pursuing PSLF, as it allows you to make lower payments while still working towards forgiveness.

Tax Bomb on Forgiven Debt

One crucial aspect to consider for IDR plans is the potential ‘tax bomb’ on forgiven debt. Currently, under current law, any loan balance forgiven under an IDR plan (after 20 or 25 years) may be considered taxable income by the IRS, with the exception of temporary relief provided by the American Rescue Plan Act, which made IDR forgiveness tax-free through 2025. It’s essential to consult with a tax professional to understand the implications for 2026 and beyond, as this can significantly impact your financial planning.

Interest Accrual and Capitalization

While IDR plans offer lower monthly payments, they often extend the repayment period, potentially leading to more interest accruing over the life of the loan. Interest capitalization occurs when unpaid interest is added to your principal balance, causing your loan to grow. The SAVE Plan significantly mitigates this with its interest subsidy, but for other IDR plans, it’s a factor to be aware of. Understanding how each plan handles interest is vital for long-term cost analysis.

Annual Recertification

If you choose an IDR plan, you will need to recertify your income and family size annually. This is crucial for keeping your payments accurate and avoiding a switch back to the Standard Repayment Plan, which could lead to significantly higher payments and interest capitalization. Missing the recertification deadline can have serious financial consequences.

Loan Consolidation

Federal student loan consolidation allows you to combine multiple federal loans into a single Direct Consolidation Loan. This can simplify your repayment by giving you one monthly payment and potentially opening up eligibility for certain IDR plans (like ICR for Parent PLUS loans) or PSLF if your original loans weren’t eligible. However, consolidation can also extend your repayment term and might cause you to lose certain borrower benefits from your original loans. Carefully weigh the pros and cons before consolidating.

How to Choose the Best Student Loan Repayment Plans for You

Selecting the ideal plan requires a personalized approach. Here’s a step-by-step guide to help you make an informed decision for 2026:

Step 1: Understand Your Loans

Log in to your studentaid.gov account to identify the types of federal loans you have (Direct Loans, FFEL, Perkins, etc.), your current balance, interest rates, and loan servicers. This information is foundational to determining your eligibility for various Student Loan Repayment Plans.

Step 2: Assess Your Current Financial Situation

Consider your current income, family size, and monthly expenses. How much can you realistically afford to pay each month without undue financial hardship? Project your income and career trajectory for the next few years. Will your income likely increase significantly, or will it remain stable?

Step 3: Evaluate Eligibility for Each Plan

Based on your loan types and financial situation, determine which IDR plans you qualify for. Use the eligibility criteria discussed above to narrow down your options. The Loan Simulator tool on studentaid.gov is an invaluable resource for this step.

Step 4: Use the Loan Simulator Tool

The Federal Student Aid (FSA) website offers a powerful Loan Simulator. This tool allows you to input your specific loan details, income, and family size to compare estimated monthly payments, total repayment costs, and potential forgiveness amounts under different plans. It’s the best way to get a clear, personalized picture.

Step 5: Consider Your Long-Term Goals

- Minimize Total Cost: If your primary goal is to pay the least amount of interest, and you can afford it, the Standard Repayment Plan is usually best.

- Lowest Monthly Payments: If affordability is your main concern, especially with a low income, the SAVE Plan is likely your best bet, followed by PAYE or IBR.

- Loan Forgiveness: If you’re pursuing PSLF or anticipate IDR forgiveness, choose a plan that offers the lowest payments while qualifying for forgiveness, such as SAVE, PAYE, or IBR.

- Career Path: If you’re in public service, prioritize plans that qualify for PSLF. If you’re in a high-earning field, you might prioritize faster repayment.

Step 6: Consult with Your Loan Servicer

Once you have a few options in mind, contact your loan servicer. They can provide personalized advice, confirm your eligibility, and help you complete the necessary paperwork to enroll or switch plans. Be prepared with your financial information and questions.

The Future of Student Loan Repayment in 2026 and Beyond

The student loan landscape is continually evolving. While the SAVE Plan provides significant relief for many, future legislative changes, economic conditions, and policy decisions could further impact available Student Loan Repayment Plans. Staying informed is paramount.

It’s wise to review your repayment strategy annually, especially when your income or family size changes, or if new legislation is passed. The goal is to remain proactive, ensuring your chosen plan continues to serve your best financial interests.

Common Mistakes to Avoid

- Ignoring Your Loans: Burying your head in the sand is the worst strategy. Proactively engage with your loans and choose a plan.

- Not Recertifying Annually: Failing to recertify your income and family size for IDR plans can lead to higher payments and capitalized interest.

- Choosing the Wrong Plan for PSLF: Only certain repayment plans qualify for PSLF. Ensure you’re on a qualifying plan if pursuing forgiveness.

- Not Understanding Interest Capitalization: Be aware of how interest can add to your principal, especially if you leave an IDR plan or no longer qualify for a partial financial hardship.

- Not Using the Loan Simulator: This free tool is invaluable for comparing options. Don’t skip it.

- Not Contacting Your Servicer: Your loan servicer is there to help. Don’t hesitate to reach out with questions.

Conclusion: Empowering Your Student Loan Journey

Navigating federal Student Loan Repayment Plans for 2026 requires diligence and informed decision-making. By understanding the intricacies of the SAVE Plan, PAYE, IBR, and ICR, you can confidently select a strategy that best fits your current financial situation and future aspirations. Remember that your repayment plan isn’t set in stone; you can switch plans as your circumstances change. The key is to stay engaged, utilize available resources like the Loan Simulator, and proactively manage your student debt.

Taking control of your student loans is a powerful step towards achieving financial stability and peace of mind. By making an educated choice today, you’re setting yourself up for a more secure financial future tomorrow.