Navigating 2026 Tax Code Changes: 5 Key Updates Affecting Your Investment Returns

Navigating 2026 Tax Code Changes: 5 Key Updates Affecting Your Investment Returns

The financial landscape is ever-evolving, and staying ahead of changes in tax legislation is paramount for any savvy investor. As we approach 2026, significant shifts in the tax code are on the horizon, poised to reshape how individuals and businesses manage their wealth and investment portfolios. These upcoming 2026 Tax Changes are not merely minor adjustments; they represent potential game-changers that could substantially impact your investment returns, retirement planning, and overall financial strategy.

Understanding these modifications well in advance allows for proactive planning, enabling you to optimize your financial decisions and mitigate any adverse effects. Failing to prepare for these shifts could lead to missed opportunities or unexpected tax liabilities. This comprehensive guide will delve into five crucial updates to the tax code, offering insights into their potential implications for your investments and providing actionable strategies to help you navigate this new terrain successfully.

From adjustments in capital gains rates to modifications in estate tax exemptions and changes affecting retirement accounts, the scope of these reforms is broad. Whether you are a seasoned investor, a small business owner, or someone simply looking to secure their financial future, the information presented here will be invaluable in formulating a robust financial plan for the years to come. Let’s explore these pivotal 2026 Tax Changes and equip ourselves with the knowledge needed to thrive in the face of fiscal evolution.

The Sunset of the Tax Cuts and Jobs Act (TCJA) Provisions

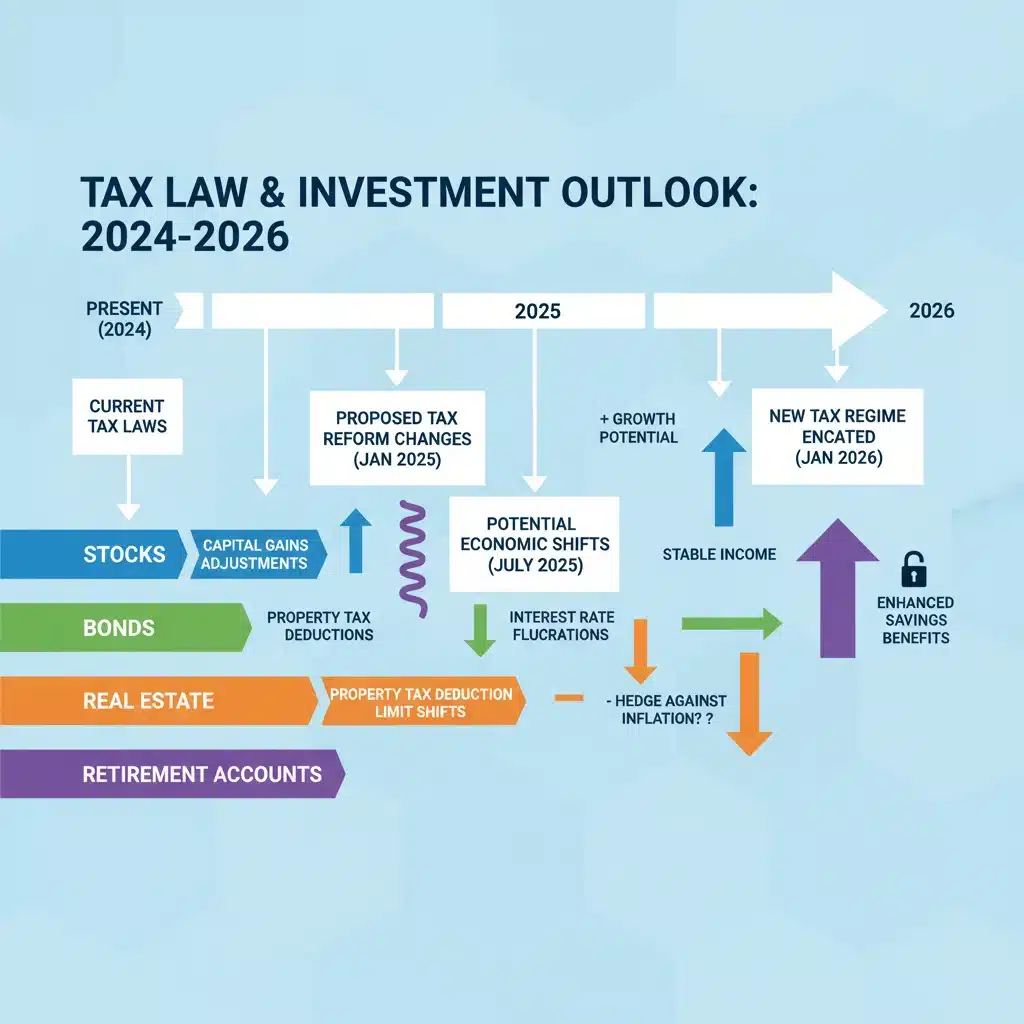

One of the most significant factors driving the anticipated 2026 Tax Changes is the scheduled sunsetting of many provisions enacted under the Tax Cuts and Jobs Act (TCJA) of 2017. Unless Congress acts to extend them, a wide array of individual income tax provisions are set to expire at the end of 2025, reverting to pre-TCJA law. This includes changes to individual income tax rates, the standard deduction, personal exemptions, and various itemized deduction limitations. For investors, these shifts can indirectly affect disposable income available for investment and directly influence the after-tax returns on their portfolios.

Specifically, we could see a return to higher marginal income tax rates for many brackets, especially for higher earners. The current seven individual income tax brackets (10%, 12%, 22%, 24%, 32%, 35%, and 37%) are expected to revert to their pre-TCJA levels, which were generally higher. For instance, the top marginal rate could climb back to 39.6%. This change has profound implications for how investment income, such as interest, dividends, and short-term capital gains, is taxed. If your ordinary income tax rate increases, the tax bite on these types of investment earnings will also rise, diminishing your net returns.

Furthermore, the standard deduction, which was significantly increased under the TCJA, is also slated to revert to lower levels, adjusted for inflation. This could mean fewer taxpayers will opt for the standard deduction, potentially leading to more individuals itemizing deductions. While this might not directly impact investment income, it affects overall taxable income and, by extension, the amount of money available for saving and investing. Understanding these foundational shifts is crucial for any comprehensive financial planning strategy as we approach the 2026 Tax Changes.

The TCJA also eliminated personal exemptions, replacing them with an expanded child tax credit. While the child tax credit is scheduled to revert, the reintroduction of personal exemptions could affect the taxable income of larger families. All these elements combined create a complex environment where careful planning becomes even more critical. Investors need to assess their current tax bracket and project how these changes might push them into a higher bracket, necessitating adjustments to their investment strategies.

For example, if you anticipate being in a higher tax bracket in 2026, you might consider accelerating income into 2025 or deferring deductions to future years. Alternatively, exploring tax-advantaged investment vehicles, such as municipal bonds or tax-deferred retirement accounts, could become even more appealing. The key takeaway here is that the sunset of TCJA provisions forms the bedrock of the upcoming 2026 Tax Changes, and its broad impact will necessitate a thorough review of personal financial strategies.

Capital Gains and Qualified Dividends Tax Rate Adjustments

One of the most direct impacts of the 2026 Tax Changes on investors will be the potential adjustments to capital gains and qualified dividends tax rates. Under current law, long-term capital gains (on assets held for more than one year) and qualified dividends are subject to preferential tax rates: 0%, 15%, or 20%, depending on the taxpayer’s ordinary income bracket. As the TCJA provisions expire, these rates are also expected to revert to their pre-TCJA structure, which could mean an increase for many investors.

Before the TCJA, the top long-term capital gains rate was 20% for those in the highest ordinary income tax bracket (39.6%). With the potential return to a 39.6% top ordinary income rate, the 20% capital gains rate would likely apply to a lower income threshold, affecting a broader range of high-income investors. Even more significantly, the thresholds for the 0% and 15% rates could also shift, potentially pushing more middle-income investors into the 15% or even 20% bracket for their long-term capital gains and qualified dividends.

Consider an investor who currently falls into the 15% long-term capital gains bracket. If the income thresholds change, they might find themselves in the 20% bracket, leading to a higher tax burden on their investment profits. This change is particularly relevant for those planning to sell appreciated assets or who receive significant qualified dividends from their stock portfolios. The timing of such sales could become a critical component of tax planning. For instance, realizing substantial capital gains in 2025 might be more advantageous than waiting until 2026, depending on the final legislative outcome.

Furthermore, the 3.8% Net Investment Income Tax (NIIT), which applies to certain unearned income for high-income individuals, will continue to apply regardless of the TCJA sunset. This tax is levied on the lesser of net investment income or the amount by which modified adjusted gross income exceeds certain thresholds ($200,000 for single filers, $250,000 for married filing jointly). With potential increases in ordinary income and capital gains rates, the combined tax on investment income for high earners could become substantially higher, making tax-efficient investing even more crucial.

Strategies to consider in light of these potential 2026 Tax Changes include tax-loss harvesting, which involves selling investments at a loss to offset capital gains and potentially a limited amount of ordinary income. Investors might also want to review their asset location strategies, placing highly taxed assets (like bonds or REITs that generate ordinary income) in tax-advantaged accounts (like 401(k)s or IRAs) and placing growth-oriented assets that generate long-term capital gains in taxable accounts, if those gains are taxed at lower rates. The objective is to minimize the overall tax drag on investment returns, ensuring that more of your earnings contribute to wealth accumulation.

Changes to Estate and Gift Tax Exemptions

Another area significantly affected by the sunset of TCJA provisions pertains to estate and gift taxes. The TCJA dramatically increased the basic exclusion amount for estate and gift taxes. For 2024, this amount stands at $13.61 million per individual ($27.22 million for a married couple). However, come January 1, 2026, without further legislative action, this exclusion amount is scheduled to revert to its pre-TCJA level, adjusted for inflation, which is projected to be approximately $7 million per individual.

This reduction in the estate and gift tax exemption is one of the most critical 2026 Tax Changes for high-net-worth individuals and families. It means that significantly more wealth could become subject to federal estate tax, which currently carries a top rate of 40%. For families with substantial assets, this change necessitates an immediate review and potential restructuring of their estate plans.

Consider a family with a net worth of $20 million. Under current law, this amount would likely fall within the combined exclusion for a married couple, incurring no federal estate tax. However, if the exclusion reverts to $7 million per individual, a married couple would have a combined exclusion of $14 million. This would leave $6 million of their estate potentially subject to the 40% federal estate tax, resulting in a tax liability of $2.4 million. This is a substantial sum that could significantly diminish the legacy passed on to heirs.

To prepare for these impending 2026 Tax Changes, individuals and families with estates exceeding the projected lower exemption amounts should consider utilizing the higher current exemption before it potentially halves. Strategies include making substantial gifts to beneficiaries now, either directly or through trusts, to take advantage of the current, more generous gift tax exclusion. For example, establishing an irrevocable trust and funding it with assets up to the current exemption amount can remove those assets from your taxable estate, effectively locking in the higher exclusion.

Another strategy involves implementing advanced estate planning techniques such as Grantor Retained Annuity Trusts (GRATs), Qualified Personal Residence Trusts (QPRTs), or charitable lead trusts. These tools can help transfer wealth to future generations or charitable organizations in a tax-efficient manner, reducing the overall size of the taxable estate. Consulting with an experienced estate planning attorney and financial advisor is crucial to determine the most appropriate strategies based on individual circumstances and family goals.

It’s important to remember that making large gifts has implications, including relinquishing control over the gifted assets. Therefore, careful consideration and professional guidance are essential. The looming reduction in estate and gift tax exemptions underscores the urgency for proactive estate planning in anticipation of the 2026 Tax Changes.

Impact on Retirement Savings and Contributions

While direct changes to contribution limits for 401(k)s, IRAs, and other retirement accounts are not explicitly tied to the TCJA sunset, the broader 2026 Tax Changes will indirectly influence retirement savings strategies. The potential increase in individual income tax rates could alter the calculus for choosing between pre-tax (traditional) and after-tax (Roth) contributions to retirement accounts.

Currently, many taxpayers benefit from the immediate tax deduction offered by traditional 401(k) and IRA contributions, especially if they are in a higher tax bracket. However, if tax rates are expected to be significantly higher in retirement, then a Roth account, where contributions are made with after-tax dollars but qualified withdrawals are tax-free in retirement, becomes more attractive. Conversely, if current tax rates are high but expected to be lower in retirement, traditional accounts might be more beneficial.

With the projected increase in marginal tax rates post-2025, many individuals might find themselves in a higher tax bracket in 2026 than they are today. This scenario generally favors Roth contributions, as paying taxes now at a lower rate (relative to future rates) on contributions could be more advantageous than deferring taxes at a potentially higher future rate. This is a critical consideration for investors evaluating their retirement savings strategy ahead of the 2026 Tax Changes.

Furthermore, the ability to make Roth conversions could also be impacted. A Roth conversion involves moving pre-tax assets from a traditional IRA or 401(k) to a Roth account, triggering income tax on the converted amount in the year of conversion. If tax rates are lower in 2025 than they are projected to be in 2026 and beyond, then 2025 might present a strategic window for executing Roth conversions at a relatively lower tax cost. This move could allow your converted assets to grow tax-free and be withdrawn tax-free in retirement, shielding them from potentially higher future tax rates.

Another aspect to consider is the impact on required minimum distributions (RMDs). While the SECURE Act 2.0 pushed back the age for RMDs, the taxability of these distributions is directly tied to your ordinary income tax rate in retirement. If future tax rates are higher due to the 2026 Tax Changes, RMDs from traditional accounts will be subject to a greater tax burden. This reinforces the appeal of Roth accounts, which are exempt from RMDs for the original owner and offer tax-free withdrawals for beneficiaries.

Reviewing your retirement savings mix, including the balance between pre-tax and Roth contributions, and evaluating the potential for Roth conversions, should be a key part of your financial planning process as these tax changes loom. Proactive adjustments can significantly enhance the tax efficiency of your retirement nest egg.

Potential for New Tax Legislation and Economic Factors

Beyond the sunsetting of TCJA provisions, the landscape of 2026 Tax Changes could also be shaped by new tax legislation. The political environment and prevailing economic conditions often serve as catalysts for further tax reform. While predicting specific new legislation is challenging, it’s essential for investors to remain vigilant and adaptable to potential additional changes that could arise from congressional action.

Historically, periods of economic growth or recession, shifts in political power, or the need to address national debt have all spurred significant tax policy debates and reforms. For instance, there could be discussions around increasing corporate tax rates, introducing new wealth taxes, or altering existing deductions and credits. Any of these could have ripple effects on investment markets and individual financial planning.

For example, proposals to increase the corporate income tax rate could impact corporate earnings and, consequently, stock valuations. If companies face higher tax burdens, their profitability might decrease, potentially leading to lower stock prices or reduced dividend payouts. Investors should monitor these discussions closely and consider how such changes might affect their equity portfolios. Diversification across various asset classes and geographies can help mitigate risks associated with specific legislative changes.

Furthermore, economic factors such as inflation and interest rates will continue to play a crucial role. High inflation can erode the purchasing power of investment returns, making tax efficiency even more critical. Rising interest rates can impact bond valuations and the cost of borrowing, influencing real estate investments and other leveraged assets. While not direct 2026 Tax Changes, these economic forces interact with tax policy to shape the real returns on your investments.

Investors should also consider the potential for changes to the qualified business income (QBI) deduction under Section 199A, which is also set to expire. This deduction allows eligible pass-through entities (sole proprietorships, partnerships, S corporations) to deduct up to 20% of their qualified business income. Its expiration would significantly impact small business owners and those with income from pass-through entities, increasing their taxable income and potentially their overall tax burden. This would necessitate a re-evaluation of business structures and income distribution strategies.

Staying informed through reputable financial news sources, consulting with tax professionals, and maintaining flexibility in your financial plan are key strategies for navigating this uncertain legislative environment. The interplay between existing tax law, sunsetting provisions, and potential new legislation makes continuous monitoring and proactive adjustment indispensable for successful investment management in the lead-up to and beyond 2026.

Proactive Strategies for Investors Ahead of 2026

Given the breadth and potential impact of the 2026 Tax Changes, adopting a proactive and well-informed approach is not just advisable, but essential. Here are several key strategies investors should consider implementing to optimize their financial position:

1. Comprehensive Financial and Tax Review

Begin by conducting a thorough review of your current financial situation, including your investment portfolio, income streams, deductions, and overall tax liability. Project your income and expenses for 2025 and beyond, considering how the anticipated 2026 Tax Changes might affect your taxable income and marginal tax rates. This foundational step will help you identify areas of vulnerability and opportunities for optimization.

2. Rebalance Investment Portfolios for Tax Efficiency

Evaluate your asset location strategy. Consider placing tax-inefficient investments (like actively managed funds with high turnover, REITs, or corporate bonds that generate ordinary income) into tax-advantaged accounts (401(k)s, IRAs, HSAs). Conversely, growth stocks and other investments expected to generate long-term capital gains might be more efficiently held in taxable accounts if their capital gains rates remain preferential or if you plan to utilize tax-loss harvesting strategies.

3. Strategic Capital Gains and Loss Management

If you anticipate higher capital gains tax rates in 2026, consider realizing some long-term capital gains in 2025, especially if you are currently in a lower tax bracket. Conversely, if you have investments with unrealized losses, consider tax-loss harvesting before the end of 2025 to offset capital gains and potentially up to $3,000 of ordinary income. This strategy can reduce your taxable income and improve your after-tax returns. Plan any significant asset sales with the upcoming tax changes in mind.

4. Maximize Retirement Contributions and Consider Roth Conversions

Maximize contributions to all available retirement accounts. If you expect to be in a higher tax bracket in 2026, increasing contributions to traditional 401(k)s or IRAs in 2025 can provide a larger deduction at potentially higher current rates. Simultaneously, consider whether a Roth conversion makes sense. If you anticipate higher tax rates in retirement, converting a portion of your traditional IRA or 401(k) to a Roth in 2025 could allow you to pay taxes on the conversion at a relatively lower rate, securing tax-free withdrawals in the future.

5. Revisit Estate and Gift Planning

For high-net-worth individuals, the impending reduction in the estate and gift tax exemption is a critical concern. If your estate is likely to exceed the projected lower exemption amount, consult with an estate planning attorney. Consider utilizing the current higher gift tax exclusion by making substantial gifts to beneficiaries or funding irrevocable trusts before the end of 2025. This could significantly reduce your future estate tax liability and ensure more of your wealth passes to your heirs as intended.

6. Stay Informed and Seek Professional Advice

Tax laws are complex and subject to change. Remaining informed about legislative developments and economic trends is crucial. More importantly, engage with qualified financial advisors, tax professionals, and estate planning attorneys. They can provide personalized advice tailored to your specific financial situation, helping you navigate the intricacies of the 2026 Tax Changes and develop robust strategies to protect and grow your wealth.

Conclusion: Preparing for the Financial Future

The upcoming 2026 Tax Changes represent a pivotal moment for investors and individuals engaged in long-term financial planning. The sunsetting of key provisions from the Tax Cuts and Jobs Act of 2017, coupled with the potential for new legislative action, creates an environment ripe for strategic re-evaluation. From adjustments in individual income and capital gains tax rates to significant shifts in estate and gift tax exemptions and indirect impacts on retirement savings, the implications are far-reaching.

Proactive planning is not merely an option but a necessity. By understanding these potential changes and implementing strategies such as comprehensive financial reviews, portfolio rebalancing for tax efficiency, strategic capital gains management, maximizing retirement contributions, and revisiting estate plans, you can position yourself to not only mitigate adverse effects but also capitalize on new opportunities.

The financial world is dynamic, and tax codes are no exception. The most successful investors are those who anticipate change, understand its potential impact, and adapt their strategies accordingly. As we move closer to 2026, the guidance of experienced financial professionals will be invaluable in navigating these complexities and ensuring your financial future remains secure and prosperous. Start your planning today to transform potential challenges into strategic advantages.

s Guide")

Limits Explained")

in 2025: Hit $23,000 Limit & Cut Taxes")