Retirement Planning 2026: Adjusting Your Portfolio for an Expected 7% Market Volatility

As we inch closer to 2026, the horizon for retirement planning presents both exciting opportunities and discernible challenges. For those eyeing retirement in the near future, or simply looking to fortify their financial future, understanding the economic landscape is paramount. Current projections hint at an expected 7% market volatility for 2026, a figure that demands careful consideration and strategic adjustments to your investment portfolio. This comprehensive guide delves into effective strategies for Retirement Planning 2026, ensuring your financial stability amidst potential market fluctuations.

Understanding the 2026 Market Volatility Landscape

Market volatility, characterized by rapid and often unpredictable price movements, is an inherent part of investing. While it can be daunting, it also presents opportunities for savvy investors. The projected 7% market volatility for 2026 isn’t just a number; it’s a signal to reassess, rebalance, and reinforce your retirement strategy. This level of volatility suggests that while growth potential might exist, so too does the risk of significant downturns. Factors contributing to this forecast include ongoing geopolitical tensions, inflation concerns, interest rate policies, technological advancements, and shifts in consumer behavior. Each of these elements can individually and collectively influence market dynamics, making robust Retirement Planning 2026 crucial.

Historically, markets have always experienced cycles of ups and downs. What makes the 2026 projection significant is the specific magnitude. A 7% fluctuation, whether upward or downward, can have a substantial impact on portfolios, especially for those nearing or in retirement who have less time to recover from losses. Therefore, simply hoping for the best is not a viable strategy. Proactive measures, informed decisions, and a clear understanding of your risk tolerance are essential components of effective Retirement Planning 2026.

It’s important to differentiate between short-term noise and long-term trends. While daily market movements can be distracting, our focus for Retirement Planning 2026 should remain on the overarching strategy that withstands these fluctuations. This involves looking beyond immediate headlines and understanding the fundamental drivers behind economic shifts. Are industries undergoing transformative changes? Are new regulatory frameworks emerging? These broader strokes often dictate the long-term viability of your investments and require a forward-thinking approach to your retirement fund management.

Assessing Your Current Retirement Portfolio

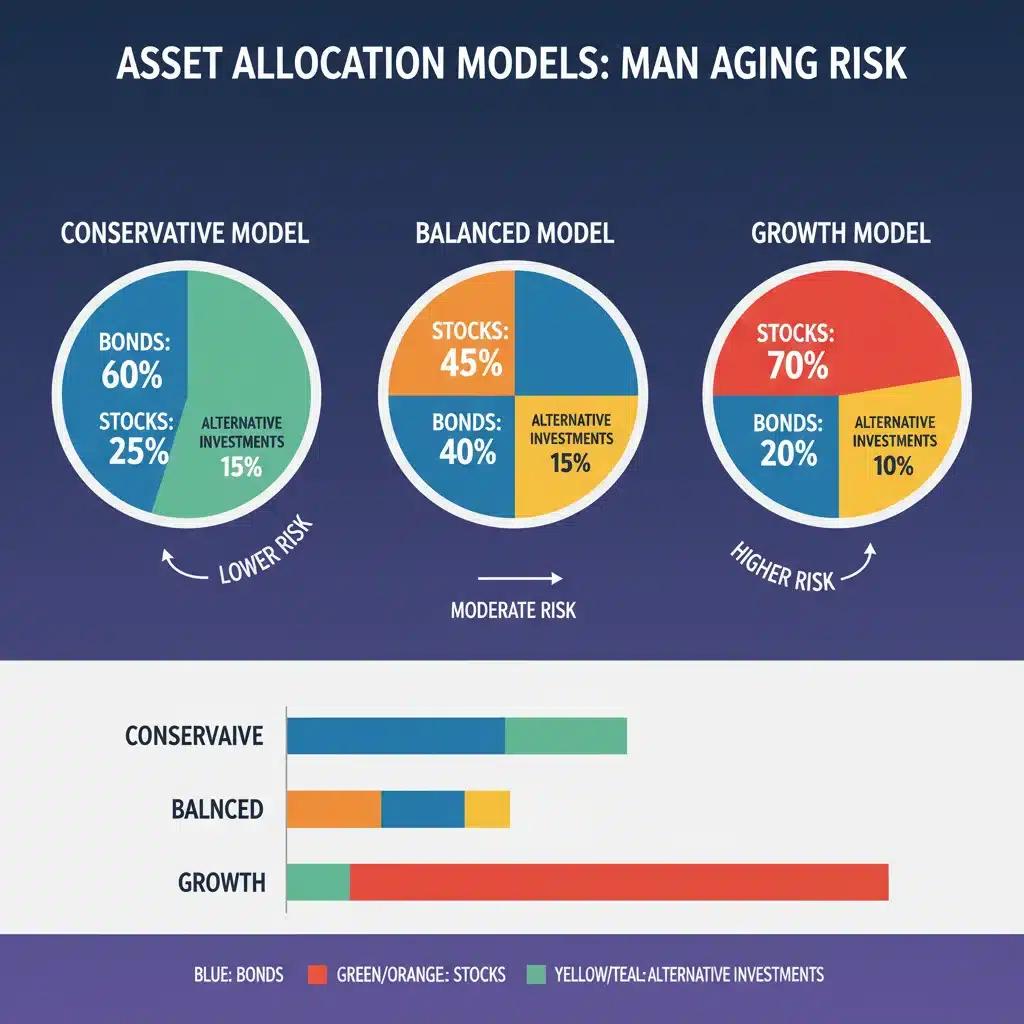

Before making any adjustments, a thorough assessment of your current retirement portfolio is imperative. This involves a detailed review of your asset allocation, risk exposure, and diversification. Ask yourself: How much of my portfolio is in stocks, bonds, real estate, and other alternative investments? What is the correlation between these assets? Are there any hidden risks or concentrations that could be detrimental in a volatile market? For effective Retirement Planning 2026, understanding your current position is the first step towards optimization.

For many, retirement portfolios often become more conservative as retirement approaches. However, a ‘set it and forget it’ mentality can be dangerous, especially with anticipated volatility. Reviewing your portfolio isn’t just about checking balances; it’s about evaluating the underlying assets and their potential performance under different market conditions. For instance, if a significant portion of your portfolio is tied to a single sector that might be particularly sensitive to economic shifts, this could expose you to undue risk. Diversification, therefore, becomes a key theme in safeguarding your assets for Retirement Planning 2026.

Consider your personal financial situation as well. Has your income changed? Are your projected retirement expenses still accurate? Have there been any major life events that might impact your financial needs? These personal factors are just as important as market conditions when it comes to assessing the suitability of your current portfolio. A holistic view, combining both market outlook and personal circumstances, will provide the clearest picture for informed decision-making in your journey towards successful Retirement Planning 2026.

Strategic Adjustments for 7% Market Volatility

Diversification Beyond the Basics

While diversification is a fundamental principle of investing, its importance amplifies in a volatile environment. For Retirement Planning 2026, consider diversifying not just across different asset classes (stocks, bonds, cash), but also within them. This means investing in various industries, geographies, and company sizes. For example, within equities, don’t just focus on large-cap tech stocks; explore small-cap value stocks, international markets, and emerging economies. This broader approach helps to spread risk and potentially capture growth from different market segments, even if one area underperforms.

Furthermore, look into alternative investments that may have a lower correlation with traditional stock and bond markets. These could include real estate (REITs), commodities, or even private equity funds, though these often come with their own set of risks and liquidity considerations. The goal is to build a portfolio that doesn’t move in lockstep with the broader market, offering some insulation during periods of heightened volatility. This nuanced approach to diversification is a cornerstone of intelligent Retirement Planning 2026.

Rebalancing Your Portfolio

Rebalancing is the process of adjusting your portfolio back to your target asset allocation. In a volatile market, some assets may grow significantly while others decline, throwing your original allocation out of whack. Regularly rebalancing ensures you’re not taking on more risk than intended. For Retirement Planning 2026, consider rebalancing more frequently, perhaps quarterly or semi-annually, rather than annually. This allows you to lock in gains and reduce exposure to overperforming (and potentially overvalued) assets, while increasing your stake in underperforming (and potentially undervalued) ones.

Automated rebalancing tools offered by many brokerage platforms can simplify this process. However, it’s crucial to understand the implications of each rebalance. Sometimes, a tactical tilt away from your standard allocation might be warranted based on market outlook, but this should be done cautiously and with professional advice. The disciplined act of rebalancing is a powerful tool for managing risk and maintaining your desired investment profile, which is critical for robust Retirement Planning 2026.

Considering Income-Generating Assets

In a volatile market, relying solely on capital appreciation can be risky. Incorporating income-generating assets can provide a steady stream of returns, helping to cushion your portfolio against market downturns. For Retirement Planning 2026, consider dividend-paying stocks, high-quality corporate bonds, government bonds, and real estate investment trusts (REITs).

Dividend stocks, particularly those from financially stable companies with a history of consistent payouts, can offer both income and potential for capital growth. Bonds, especially those with higher credit ratings, can provide stability and predictable income, although their yields may fluctuate with interest rates. REITs, which invest in income-producing real estate, can also offer attractive dividends and diversification benefits. These income streams can be particularly valuable for retirees who rely on their portfolios for living expenses, providing a sense of financial security even when market values are declining. This strategy is an integral part of resilient Retirement Planning 2026.

Risk Management Techniques

Effective risk management goes beyond diversification. For Retirement Planning 2026, explore techniques such as dollar-cost averaging, which involves investing a fixed amount regularly, regardless of market fluctuations. This strategy helps to reduce the average cost of your investments over time and mitigates the risk of investing a large sum at an unfavorable market peak.

Another technique is to maintain an adequate cash reserve. This cash can serve as a buffer for unexpected expenses or as dry powder to take advantage of market dips. The amount of cash you should hold depends on your personal circumstances, but generally, having 6-12 months of living expenses in an easily accessible, low-risk account is a good starting point. This liquidity provides peace of mind and reduces the need to sell investments at a loss during a downturn, a crucial aspect of mindful Retirement Planning 2026.

Furthermore, consider stop-loss orders for individual stock holdings if you are actively managing your portfolio. While not foolproof, these orders can help limit potential losses by automatically selling a security if it drops to a certain price. However, be aware of market gaps where prices can fall below your stop-loss without triggering the sale. For index funds and broad market ETFs, this strategy is less applicable, but for specific stock picks, it can be a valuable risk mitigation tool. These proactive risk management steps are vital for successful Retirement Planning 2026.

The Role of Professional Guidance in Retirement Planning 2026

Navigating an expected 7% market volatility can be complex, and the stakes are high, especially when it concerns your retirement. Engaging with a qualified financial advisor can provide invaluable insights and personalized strategies. A good advisor can help you:

- Assess Your Risk Tolerance: A professional can objectively evaluate your true risk tolerance, which might differ from your perceived tolerance, especially during volatile periods.

- Tailor a Portfolio Strategy: Based on your individual goals, timeline, and risk profile, an advisor can help construct a portfolio specifically designed for Retirement Planning 2026 and beyond.

- Monitor and Adjust: They can continuously monitor market conditions and your portfolio’s performance, making timely adjustments as needed to keep you on track.

- Tax-Efficient Strategies: Advisors can help implement tax-efficient withdrawal strategies and investment vehicles, maximizing your net returns.

- Emotional Discipline: During volatile times, emotions can lead to poor investment decisions. An advisor can provide a rational perspective and help you stick to your long-term plan.

Finding an advisor who understands your specific needs for Retirement Planning 2026 and has experience navigating volatile markets is crucial. Look for certified financial planners (CFP®) or fiduciaries who are legally bound to act in your best interest. Their expertise can be the difference between a secure retirement and one fraught with uncertainty.

Long-Term Perspective and Patience

Despite the focus on 2026 volatility, it’s crucial to maintain a long-term perspective. Retirement planning is a marathon, not a sprint. Market downturns, while uncomfortable, are often temporary. Historically, markets have recovered from every major correction and gone on to reach new highs. Panic selling during a downturn can lock in losses and prevent you from participating in the subsequent recovery, severely impacting your Retirement Planning 2026 goals.

Patience is a virtue in investing. Stick to your well-thought-out plan, trust in your diversified portfolio, and resist the urge to make impulsive decisions based on short-term market noise. Regularly review your financial plan, but avoid constantly tinkering with your investments. For many, simply staying invested through the ups and downs has proven to be a more effective strategy than trying to time the market. This disciplined approach is fundamental to successful Retirement Planning 2026.

Remember that the projected 7% volatility is an expectation, not a certainty. Markets are dynamic, and unforeseen events can always shift the landscape. Therefore, building a flexible and adaptable retirement plan is key. This flexibility allows you to pivot when necessary without completely abandoning your core strategy. A resilient plan for Retirement Planning 2026 will account for various scenarios and allow for adjustments without derailing your overall objectives.

Retirement Income Strategies in a Volatile Environment

For those already in retirement or very close to it, managing income in a volatile market becomes even more critical. The sequence of returns risk – the risk that poor investment returns early in retirement significantly deplete your nest egg – is a major concern. To mitigate this for Retirement Planning 2026, consider strategies like:

- Bucket Strategy: This involves segmenting your retirement funds into different ‘buckets’ based on when you’ll need the money. Short-term needs (1-3 years) are covered by cash or highly liquid assets, mid-term needs (3-10 years) by bonds, and long-term needs (10+ years) by equities. This ensures you don’t have to sell stocks at a loss to cover immediate expenses during a downturn.

- Dynamic Withdrawal Strategy: Instead of a fixed withdrawal rate, adjust your withdrawals based on market performance. In good years, you might withdraw slightly more; in down years, you might reduce your withdrawals or draw from your cash reserves. This flexibility helps your portfolio last longer.

- Annuities: While often complex, certain types of annuities can provide a guaranteed income stream for life, regardless of market performance. They can act as a valuable floor for your retirement income, reducing reliance on a volatile portfolio. However, it’s crucial to understand their fees, terms, and liquidity constraints.

- Part-time Work: For some, working part-time in early retirement can provide supplemental income, reducing the pressure on your investment portfolio during volatile periods. This extra income can allow your investments more time to recover and grow.

These strategies are designed to provide a degree of predictability and stability to your retirement income, even when the market is turbulent. They are essential considerations for effective Retirement Planning 2026, especially for those drawing income from their savings.

Monitoring Economic Indicators and Market Signals

Staying informed about key economic indicators and market signals is another vital aspect of proactive Retirement Planning 2026. While you shouldn’t react to every piece of news, understanding the broader economic trends can help you anticipate potential shifts and make informed decisions. Key indicators to watch include:

- Inflation Rates: High inflation can erode purchasing power and impact the real returns of your investments.

- Interest Rates: Changes in interest rates by central banks can affect bond prices, borrowing costs, and the attractiveness of different asset classes.

- GDP Growth: Gross Domestic Product (GDP) provides an overall picture of economic health. Slower growth can signal potential market weakness.

- Employment Data: Strong employment numbers typically indicate a healthy economy, while rising unemployment can be a precursor to economic slowdowns.

- Corporate Earnings: The earnings reports of major companies can offer insights into the health of specific sectors and the overall market.

- Geopolitical Developments: International events can have significant and sometimes unpredictable impacts on global markets.

By keeping an eye on these indicators, you can better understand the context of the 7% market volatility and make more strategic decisions for your Retirement Planning 2026. This doesn’t mean becoming an economist, but rather having a general awareness of the forces shaping the financial world.

The Importance of a Written Financial Plan

Perhaps one of the most overlooked yet crucial elements of successful Retirement Planning 2026 is having a written financial plan. A well-documented plan serves as a roadmap, outlining your goals, strategies, risk tolerance, asset allocation, and withdrawal plan. It provides clarity and direction, especially when market volatility creates uncertainty.

A written plan helps you:

- Stay Focused: It reminds you of your long-term objectives, preventing emotional reactions to short-term market swings.

- Measure Progress: You can regularly review your plan to see if you’re on track and make adjustments as needed.

- Communicate with Your Advisor: It provides a clear basis for discussions with your financial advisor.

- Provide Peace of Mind: Knowing you have a structured plan in place can reduce anxiety during volatile periods.

Think of your written plan as the anchor for your Retirement Planning 2026 strategy. It should be a living document, reviewed and updated periodically, especially after significant life events or changes in market outlook. This commitment to a tangible plan is a hallmark of disciplined and successful financial management.

Conclusion: Proactive Steps for a Secure Retirement in 2026

The prospect of 7% market volatility in 2026 might seem daunting, but with proactive planning and strategic adjustments, it doesn’t have to derail your retirement dreams. By thoroughly assessing your current portfolio, diversifying intelligently, rebalancing regularly, incorporating income-generating assets, and applying sound risk management techniques, you can build a resilient retirement fund. The role of professional guidance cannot be overstated, providing the expertise and emotional discipline needed to navigate complex market conditions. Maintaining a long-term perspective, practicing patience, and developing robust retirement income strategies are equally vital.

Ultimately, successful Retirement Planning 2026 is about being prepared, adaptable, and informed. It’s about taking control of your financial future rather than leaving it to chance. Start today by reviewing your current situation, consulting with a financial expert, and implementing the strategies discussed. Your secure and comfortable retirement is worth the effort.

s Guide")