2026 Mortgage Rates: 0.5% Impact on Monthly Payments Explained

Even a seemingly minor 0.5% difference in 2026 mortgage rates can lead to hundreds of dollars in monthly payment variations, profoundly influencing a homeowner’s budget and long-term financial commitment.

Understanding the nuances of 2026 mortgage rates is crucial for anyone considering homeownership or refinancing. A slight shift, perhaps just 0.5%, can surprisingly translate into significant monthly payment differences, potentially saving or costing you hundreds of dollars over the lifetime of your loan.

The Basics of Mortgage Rates and Their Fluctuation

Mortgage rates are not static; they are dynamic economic indicators influenced by a myriad of factors, both domestic and global. For prospective homeowners in 2026, comprehending these underlying forces is paramount to making informed decisions. Even a seemingly small percentage point change can have substantial financial implications.

Several key elements contribute to the ebb and flow of mortgage rates. These include the Federal Reserve’s monetary policy, inflation expectations, the overall health of the U.S. economy, and the demand for mortgage-backed securities. Geopolitical events and global economic shifts can also play a role, adding layers of complexity to rate predictions.

Federal Reserve Policy and Its Influence

The Federal Reserve’s actions are often the primary driver behind short-term interest rate movements, which in turn affect mortgage rates. When the Fed raises or lowers the federal funds rate, it impacts the cost of borrowing for banks, and these costs are then passed on to consumers through various loan products, including mortgages.

- Interest Rate Hikes: Typically lead to higher mortgage rates as the cost of capital increases for lenders.

- Interest Rate Cuts: Can result in lower mortgage rates, making borrowing more affordable.

- Quantitative Easing/Tightening: Directly influences the supply and demand for mortgage-backed securities, thereby affecting their yields.

Understanding the Fed’s stance on monetary policy can provide valuable clues about the future direction of mortgage rates. Economic reports and statements from Fed officials are closely watched by market participants for any indication of upcoming changes.

Inflation and Economic Growth

Inflation is another critical factor. Lenders anticipate future inflation when setting interest rates. If inflation is expected to rise, lenders will demand higher interest rates to compensate for the reduced purchasing power of future repayments. Conversely, low inflation can lead to more favorable rates.

The strength of the economy also plays a role. A robust economy often brings higher demand for loans and potential inflationary pressures, which can push rates up. A weaker economy might see lower rates as central banks try to stimulate growth.

In conclusion, mortgage rates are a complex interplay of monetary policy, inflation, and economic conditions. Staying informed about these factors is essential for anyone navigating the 2026 housing market, as even minor fluctuations can significantly impact long-term financial commitments.

The Power of Half a Percent: A Financial Illustration

It’s easy to dismiss a 0.5% difference in interest rates as insignificant, but when applied to a large sum like a mortgage, its impact becomes remarkably substantial. This seemingly small percentage can translate into thousands of dollars over the life of a loan, affecting everything from your monthly budget to your long-term wealth accumulation. Let’s break down how this seemingly minor difference can create major financial ripples.

Consider a typical home purchase in the United States. The median home price can vary significantly by region, but for illustrative purposes, let’s assume a loan amount of $350,000. This figure is representative of many first-time homebuyers or those looking to upgrade in various markets across the country.

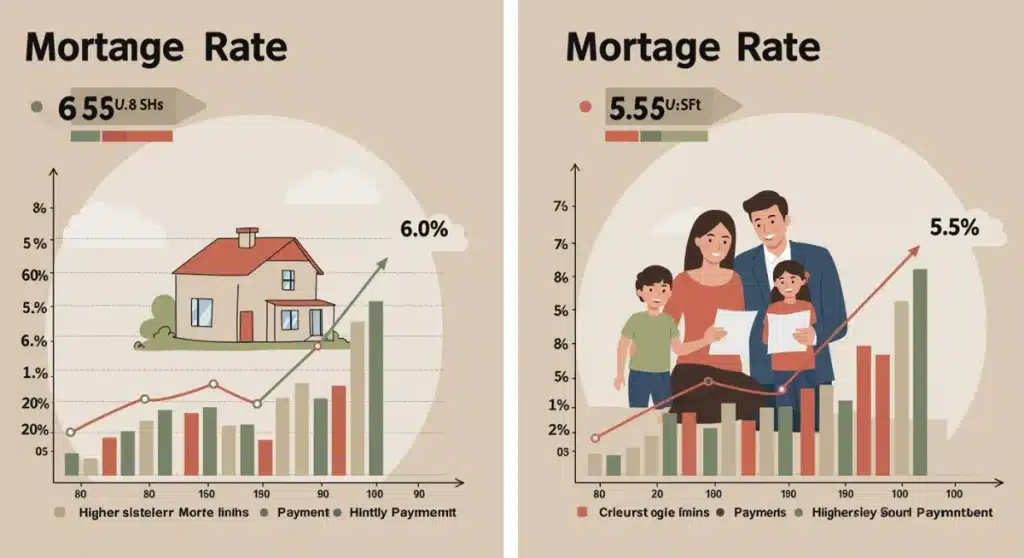

Scenario 1: Mortgage Rate at 6.0%

With a 30-year fixed-rate mortgage of $350,000 at an interest rate of 6.0%:

- Principal & Interest Payment: Approximately $2,098 per month.

- Total Interest Paid Over 30 Years: Roughly $405,280.

- Total Repayment Amount: Approximately $755,280.

This payment structure represents a common baseline for many borrowers. The monthly outlay feels manageable, but the long-term interest cost is substantial, as is typical for a 30-year loan.

Scenario 2: Mortgage Rate at 5.5%

Now, let’s look at the same $350,000 loan over 30 years, but with a slightly lower interest rate of 5.5%:

- Principal & Interest Payment: Approximately $1,987 per month.

- Total Interest Paid Over 30 Years: Roughly $365,320.

- Total Repayment Amount: Approximately $715,320.

The difference from just half a percentage point is immediately apparent. The monthly payment drops significantly, and the total interest paid over the loan’s duration is substantially less.

The comparison between these two scenarios clearly illustrates the profound financial impact of a 0.5% difference in 2026 mortgage rates. The monthly savings of $111 ($2,098 – $1,987) might seem modest on their own, but when compounded over 30 years, they amount to a staggering $39,960 in total interest saved. This nearly $40,000 could be used for retirement savings, home improvements, or other investments, highlighting the critical importance of securing the best possible rate.

Understanding the True Cost: Beyond Monthly Payments

While the monthly payment is the most immediate and tangible impact of mortgage rates, focusing solely on this figure can be misleading. The true cost of a mortgage extends far beyond the recurring monthly outlay, encompassing the total interest paid over the loan’s lifetime, opportunity costs, and the overall financial flexibility it affords or restricts. A slight difference in 2026 mortgage rates can compound these effects, creating a much larger financial disparity over time.

Many homeowners tend to fixate on the affordability of the monthly payment, often overlooking the long-term implications of their interest rate. This short-sighted view can lead to decisions that cost them tens of thousands of dollars, or even more, in unnecessary interest payments.

Total Interest Paid: The Hidden Cost

As illustrated in the previous section, the total interest paid over a 30-year mortgage can be a colossal figure. A 0.5% difference can subtract or add nearly $40,000 to this amount. This sum represents money that could have been invested, used for educational expenses, or contributed to a more robust retirement fund.

- Lower Rate Advantage: Less interest paid means more of your monthly payment goes towards the principal, building equity faster.

- Higher Rate Disadvantage: More interest paid means a slower equity build-up and a larger overall financial burden.

- Opportunity Cost: The money saved from a lower interest rate could be invested, potentially growing into a much larger sum over decades.

The long-term impact on your net worth is undeniable. Every dollar saved on interest is a dollar that can work harder for you elsewhere, contributing to your financial independence.

Impact on Equity and Wealth Building

Building equity in your home is a primary goal for many homeowners. Equity represents the portion of your home that you truly own, free and clear of the mortgage. A lower interest rate means that a greater percentage of your early payments goes towards reducing the principal balance, accelerating your equity accumulation.

Faster equity build-up provides several benefits:

- Increased Financial Security: A larger equity cushion offers more stability in case of financial hardship or market downturns.

- Access to Home Equity Loans: More equity can provide greater access to home equity loans or lines of credit for future needs like renovations or debt consolidation.

- Faster Path to Debt-Free Living: Accelerating principal repayment shortens the time until your home is fully paid off, freeing up significant cash flow for other financial goals.

In essence, the true cost of a mortgage transcends the monthly statement. It’s about the total financial commitment, the lost opportunities, and the pace at which you build wealth. Paying close attention to 2026 mortgage rates and striving for the lowest possible rate is a strategic move that pays dividends for decades.

Strategies to Secure Favorable 2026 Mortgage Rates

Navigating the mortgage market to secure the best possible rate requires a proactive and informed approach. While external economic factors are beyond a borrower’s control, several personal financial strategies can significantly influence the interest rate offered by lenders. Understanding these strategies is key to minimizing the impact of potential rate fluctuations in 2026.

Borrowers who take the time to prepare their finances and comparison shop are often rewarded with more favorable terms. The goal is to present yourself as the least risky borrower possible, thereby qualifying for the lowest available rates.

Improving Your Credit Score

Your credit score is one of the most critical factors lenders consider when determining your mortgage interest rate. A higher credit score signals to lenders that you are a responsible borrower with a strong history of repaying debts, reducing their perceived risk. This translates directly into better interest rate offers.

- Check Your Credit Report: Regularly review your credit reports from all three major bureaus (Equifax, Experian, TransUnion) for errors.

- Pay Bills on Time: Payment history is the most significant component of your credit score.

- Reduce Debt: Lowering your credit utilization ratio (the amount of credit you’re using compared to your total available credit) can boost your score.

- Avoid New Credit: Refrain from opening new credit accounts or making large purchases on credit before applying for a mortgage.

Aim for a FICO score of 740 or higher to qualify for the most competitive rates. Even a small increase in your score can lead to a noticeable reduction in your interest rate.

Increasing Your Down Payment

A larger down payment signals greater commitment and reduces the loan-to-value (LTV) ratio, which is another key factor for lenders. A lower LTV means less risk for the lender, often resulting in a more attractive interest rate. It also reduces the amount you need to borrow, which can further lower your monthly payments.

While a 20% down payment is often cited as ideal to avoid private mortgage insurance (PMI), any amount above the minimum required can be beneficial. Even putting down 10% instead of 5% can make a difference in your rate and overall loan terms.

Shopping Around for Lenders

This is perhaps one of the most overlooked yet effective strategies. Different lenders have different overhead costs, risk assessments, and pricing models, leading to variations in the rates they offer. Obtaining quotes from multiple lenders can reveal significant discrepancies, often more than the 0.5% difference we’ve been discussing.

- Compare Offers: Get at least three to five quotes from various banks, credit unions, and online lenders.

- Look Beyond the Rate: Also compare origination fees, closing costs, and other associated charges.

- Negotiate: Don’t be afraid to use a better offer from one lender to negotiate with another.

By diligently applying these strategies, prospective homebuyers in 2026 can significantly improve their chances of securing favorable 2026 mortgage rates, thereby saving money and enhancing their long-term financial outlook.

The Role of Economic Forecasts in 2026 Mortgage Decisions

Making informed mortgage decisions in 2026 requires more than just understanding current rates; it demands an eye toward the future. Economic forecasts play a pivotal role in anticipating how mortgage rates might trend, offering valuable insights that can guide buyers and refinancers. These predictions, while not guarantees, help individuals strategize their home financing plans to capitalize on favorable conditions or mitigate risks.

Various economic indicators and expert analyses contribute to these forecasts. Understanding what these indicators suggest can empower you to make timely and advantageous decisions regarding your mortgage.

Key Economic Indicators to Watch

Several economic data points are closely monitored by financial analysts and lenders to predict future interest rate movements. Keeping an eye on these can provide an early warning system for potential shifts in 2026 mortgage rates.

- Inflation Reports: The Consumer Price Index (CPI) and Producer Price Index (PPI) indicate inflationary pressures. Sustained high inflation often leads to higher rates.

- Employment Data: Strong job growth and low unemployment rates can signal a robust economy, potentially leading to rate hikes as the Fed might try to cool down an overheating economy.

- GDP Growth: A healthy Gross Domestic Product (GDP) indicates economic expansion, which can also influence the Fed’s stance on interest rates.

- Treasury Yields: The yield on 10-year Treasury bonds is often a strong predictor of long-term mortgage rates. When Treasury yields rise, mortgage rates tend to follow.

These indicators collectively paint a picture of the economic landscape, helping to forecast the direction of interest rates.

Expert Predictions and Market Sentiment

Beyond raw data, the interpretations of economic experts and overall market sentiment significantly influence mortgage rate trends. Major financial institutions, economic think tanks, and housing market analysts regularly publish their predictions for future rates.

These forecasts often consider a broader range of factors, including global economic stability, geopolitical events, and technological advancements. While predictions can vary, identifying a consensus among reputable sources can provide a more reliable outlook.

It’s important to remember that forecasts are not infallible. Unexpected events can swiftly alter the economic landscape and, consequently, mortgage rates. Therefore, continuous monitoring and flexibility in your financial planning are crucial.

In summary, integrating economic forecasts into your mortgage decision-making process for 2026 is a strategic move. By staying attuned to key indicators and expert analyses, you can position yourself to secure the most advantageous rates and effectively manage your long-term financial commitments.

Refinancing Opportunities and When to Consider Them

For current homeowners, the discussion around 2026 mortgage rates isn’t just about new purchases; it also extends to refinancing opportunities. Refinancing can be a powerful tool to reduce monthly payments, lower total interest costs, or access home equity. However, deciding when to refinance requires careful consideration of current market conditions, personal financial goals, and the costs associated with the process.

A 0.5% difference in interest rates can be a significant trigger for refinancing, especially for those who secured their original mortgage during a period of higher rates. This seemingly small change can unlock substantial savings over the remaining life of the loan.

Evaluating the Break-Even Point

One of the first steps in determining if refinancing is worthwhile is to calculate your break-even point. This is the amount of time it will take for the savings from a lower interest rate to offset the closing costs associated with the refinance. If you plan to stay in your home beyond this break-even period, refinancing may be financially beneficial.

Closing costs for a refinance can range from 2% to 5% of the loan amount, so it’s crucial to factor these into your calculations. A mortgage calculator can help you estimate both your potential savings and your break-even point accurately.

Reasons to Consider Refinancing

While a lower interest rate is the most common reason to refinance, there are several other compelling motivations:

- Lower Your Monthly Payment: Even a 0.5% rate reduction can significantly decrease your monthly outlay, freeing up cash flow.

- Reduce Total Interest Paid: A lower rate over the life of the loan means paying substantially less interest overall.

- Change Loan Term: You might refinance from a 30-year to a 15-year mortgage to pay off your home faster, or extend a 15-year to a 30-year for lower monthly payments.

- Convert Loan Type: Switching from an adjustable-rate mortgage (ARM) to a fixed-rate mortgage can provide stability and predictability in payments.

- Cash-Out Refinance: Accessing your home equity to fund major expenses like home renovations, education, or debt consolidation.

It’s important to weigh these benefits against the costs and your long-term financial plans. A careful analysis will help you decide if refinancing is the right move for you in 2026.

Long-Term Financial Planning with Varied Mortgage Rates

The impact of 2026 mortgage rates extends far beyond the immediate monthly payment; it plays a critical role in long-term financial planning and wealth accumulation. Understanding how different interest rates affect your overall financial trajectory can help you make strategic decisions that secure your financial future. A small difference today can translate into significant gains or losses over decades.

Integrating mortgage rate considerations into your broader financial strategy involves looking at your budget, investment goals, and retirement plans through the lens of your housing costs. This holistic approach ensures that your mortgage works in harmony with your other financial objectives.

Budgeting for Fluctuations and Savings

Even with a fixed-rate mortgage, other housing-related costs can fluctuate (property taxes, insurance). However, the principal and interest portion remains stable. A lower mortgage rate, secured through careful planning, frees up more disposable income. This extra cash flow can be allocated to various financial goals.

- Emergency Fund: Build or bolster your emergency savings, typically 3-6 months of living expenses.

- Debt Reduction: Pay down high-interest consumer debt faster, like credit card balances or personal loans.

- Investment Opportunities: Direct savings into retirement accounts (401(k), IRA) or other investment vehicles, leveraging the power of compounding.

By strategically allocating the savings from a lower mortgage payment, you can significantly accelerate your progress towards financial independence.

Impact on Retirement and Investment Strategies

The money saved from a lower mortgage rate doesn’t just disappear; it can be strategically employed to boost your retirement savings. For example, if you save $111 per month due to a 0.5% lower rate, investing that amount consistently over 30 years could yield a substantial sum, thanks to compound interest.

Consider the potential:

- Increased Retirement Contributions: Max out your 401(k) or IRA contributions, taking advantage of tax benefits and long-term growth.

- Diversified Portfolio: Use the extra funds to diversify your investment portfolio, reducing risk and potentially increasing returns.

- Earlier Retirement: Accelerated savings can potentially allow for an earlier retirement, or a more comfortable one.

Conversely, a higher mortgage rate means more of your income is tied up in housing costs, potentially limiting your ability to save and invest for retirement. This can delay financial goals and reduce your overall wealth accumulation.

Building Generational Wealth

For many, homeownership is a cornerstone of building generational wealth. A lower mortgage rate facilitates quicker equity build-up and a faster path to owning your home outright. This asset can then be passed down, serving as a significant financial legacy.

The decision made regarding your 2026 mortgage rates today can therefore have profound implications not just for your own financial well-being, but for future generations as well. It underscores the importance of thorough research and strategic action when securing home financing.

Government Programs and Assistance for Homebuyers in 2026

For many prospective homebuyers in 2026, navigating the complexities of mortgage rates and down payments can be daunting. Fortunately, numerous government programs and assistance initiatives exist to make homeownership more accessible, especially for first-time buyers or those with specific needs. These programs can often help mitigate the impact of higher interest rates or reduce the upfront financial burden, making a significant difference in overall affordability.

Understanding the landscape of available assistance is crucial, as these programs can offer lower interest rates, down payment assistance, or relaxed credit requirements, all of which can be pivotal in securing a home loan.

Federal Housing Administration (FHA) Loans

FHA loans are insured by the Federal Housing Administration and are designed to help low-to-moderate-income borrowers, particularly first-time homebuyers, achieve homeownership. These loans typically feature more lenient credit requirements and allow for lower down payments compared to conventional loans.

- Low Down Payment: Often as low as 3.5% of the purchase price.

- Flexible Credit Standards: More forgiving for borrowers with less-than-perfect credit scores.

- Competitive Interest Rates: While not always the lowest, FHA rates are often competitive and accessible.

It’s important to note that FHA loans require mortgage insurance premiums (MIP), both upfront and annually, which adds to the overall cost. However, for many, the benefits of easier qualification outweigh this additional expense.

VA Loans for Veterans and Service Members

For eligible veterans, active-duty service members, and surviving spouses, VA loans offer exceptional benefits. These loans are guaranteed by the U.S. Department of Veterans Affairs and are among the most advantageous mortgage options available.

- No Down Payment Required: One of the most significant benefits, allowing borrowers to finance 100% of the home’s value.

- No Private Mortgage Insurance (PMI): Eliminates a significant monthly cost associated with low down payments on other loan types.

- Competitive Interest Rates: Often among the lowest available due to the government guarantee.

VA loans also have limits on closing costs and do not penalize borrowers for early payoff, making them a highly attractive option for the military community.

USDA Rural Development Loans

The U.S. Department of Agriculture (USDA) offers loans aimed at promoting homeownership in designated rural and suburban areas. These loans are designed for low-to-moderate-income individuals and families who may not qualify for traditional mortgages.

- No Down Payment: Similar to VA loans, USDA direct and guaranteed loans can offer 100% financing.

- Low Mortgage Insurance: While required, the mortgage insurance premiums are typically lower than those for FHA loans.

- Income and Location Restrictions: Eligibility is tied to income limits and the property’s location within eligible rural areas.

Exploring these government-backed programs is a vital step for many first-time homebuyers or those with specific eligibility criteria in 2026. They can significantly reduce the financial hurdles to homeownership and help secure more favorable terms, even when facing fluctuating 2026 mortgage rates.

| Key Aspect | Impact of 0.5% Rate Difference |

|---|---|

| Monthly Payment | Can change by hundreds of dollars, affecting immediate budget. |

| Total Interest Paid | Tens of thousands of dollars difference over the loan’s lifetime. |

| Equity Building | Faster or slower equity growth, impacting wealth accumulation. |

| Financial Flexibility | More or less disposable income for savings, investments, or debt. |

Frequently Asked Questions About 2026 Mortgage Rates

General economic conditions significantly influence 2026 mortgage rates. A strong economy with low unemployment and moderate inflation may lead to higher rates as the Federal Reserve potentially tightens monetary policy. Conversely, economic slowdowns or recession fears often result in lower rates to stimulate borrowing and investment.

While specific requirements vary by lender, a credit score of 740 or higher is generally considered excellent for securing the most competitive 2026 mortgage rates. Scores between 620-740 can still qualify for loans, but often at slightly higher interest rates, impacting monthly payments.

Absolutely. For a typical $350,000, 30-year mortgage, a 0.5% rate difference can save you nearly $40,000 in total interest paid over the life of the loan. This translates to substantial savings that can be redirected to other financial goals, highlighting the importance of rate shopping.

The choice between fixed-rate and adjustable-rate mortgages (ARMs) in 2026 depends on your risk tolerance and market outlook. Fixed rates offer payment stability, ideal if rates are expected to rise. ARMs might offer lower initial rates but carry the risk of future payment increases if rates climb, making them suitable for short-term homeowners.

Several government programs can assist first-time homebuyers with 2026 mortgage rates. FHA loans offer low down payments and flexible credit requirements. VA loans provide no down payment options for veterans. USDA loans support rural homebuyers. These programs often come with competitive rates, making homeownership more accessible.

Conclusion

The detailed exploration of 2026 mortgage rates clearly demonstrates that even a seemingly minor 0.5% difference carries profound financial implications. From altering monthly payments by hundreds of dollars to affecting tens of thousands in total interest paid over the life of a loan, every fraction of a percentage point matters. Proactive financial planning, strong credit, and diligent rate shopping are indispensable strategies for securing the most favorable terms. Understanding the broader economic landscape and leveraging available government assistance programs can further empower homebuyers and refinancers to make astute decisions, ultimately shaping their long-term financial health and wealth accumulation. The journey to homeownership in 2026 demands informed choices, recognizing that a small rate difference today can lead to substantial financial benefits or burdens tomorrow.